How much of your finance team’s potential is currently buried under a mountain of unposted receipts and spreadsheet rows that refuse to match? If your month-end close feels more like a frantic rescue mission than a standard procedure, you aren’t alone. Most UK finance leaders still lose days to manual data entry, yet with the 2026 FCA reconciliation rules now in full effect, the margin for error has vanished. Transitioning to automated credit card reconciliation software is no longer just an efficiency play; it’s a necessity for maintaining compliance and visibility in an increasingly regulated market.

We understand the frustration of fragmented data and the persistent dread of VAT categorisation errors. You deserve a process that flows with the speed of your business rather than acting as a bottleneck. This guide will show you how to eliminate manual matching and achieve a “one-click” month-end close by training AI to mirror your specific business intelligence. We’ll explore the 2026 UK finance landscape, from the latest Open Finance roadmaps to seamless integrations with platforms like Xero and Sage, ensuring your team can scale without the need to increase headcount.

Key Takeaways

- Identify the hidden productivity drains of manual matching and why 2026 regulatory shifts make spreadsheets a high-risk strategy for UK finance teams.

- Learn how automated credit card reconciliation software utilises intelligent pattern recognition to move beyond simple, error-prone rules.

- Evaluate essential features like OCR accuracy and deep integration to ensure your automation platform speaks the same language as Xero or Sage.

- Follow a clear, step-by-step implementation guide to map your Chart of Accounts and secure real-time Open Banking bank feeds.

- Discover how to achieve a “one-click” month-end close and gain strategic spend analytics that empower your board-level decision-making.

The Growing Cost of Manual Credit Card Reconciliation in 2026

In 2026, relying on manual spreadsheets is no longer just a slow way of working; it’s a liability. UK finance teams face increased pressure from the Financial Services & Markets Bill 2026, which demands unprecedented levels of transparency and outcomes-based regulation. If your team is still manually matching transactions, you’re likely missing the forest for the trees. Deploying automated credit card reconciliation software is the only way to ensure your data remains audit-ready whilst your team focuses on high-value forecasting.

The fundamental process of reconciliation serves as the backbone of financial integrity. However, when this process relies on human entry, the cost of “getting it right” becomes astronomical. High-level accountants shouldn’t spend their valuable hours cross-referencing corporate card statements against fragmented bank feeds. This manual labour prevents them from performing the strategic analysis that actually drives business growth. It’s a hidden drain on productivity that keeps your most expensive talent tethered to low-value tasks.

The “Spreadsheet Trap” and Compliance Risks

Spreadsheets are often viewed as a “safe” default, but they’re inherently fragile. A single cell error or a miscalculated VAT categorisation can trigger an HMRC audit red flag, especially with the strict quarterly updates required for Making Tax Digital. The risk is compounded by the psychological toll of repetitive tasks. Talented professionals don’t want to spend their careers fixing broken formulas. It’s a sure-fire way to increase staff turnover in a market where fintech vacancies are growing by 14% annually. You can read more about why these habits are dangerous in our guide on The True Cost of Manual Reconciliation: Busting the Myth of the “Safe” Spreadsheet.

Fragmented Data: The Enemy of the Modern CFO

Remote and hybrid working models have complicated the receipt-chasing process amongst dispersed teams. When data is scattered across Slack channels, email threads, and physical pockets, the CFO loses real-time visibility. This fragmentation makes it impossible to provide accurate spend analytics during board meetings. By the time the numbers are reconciled, the data is already out of date. 2026 regulatory standards, such as the new FCA daily safeguarding rules for payment firms, require a speed of reporting that manual processes simply can’t match. Reconciliation friction is the primary barrier to finance team scalability. Implementing automated credit card reconciliation software removes this friction, allowing your function to grow without an exponential increase in headcount.

How AI-Driven Reconciliation Software Transforms Finance Workflows

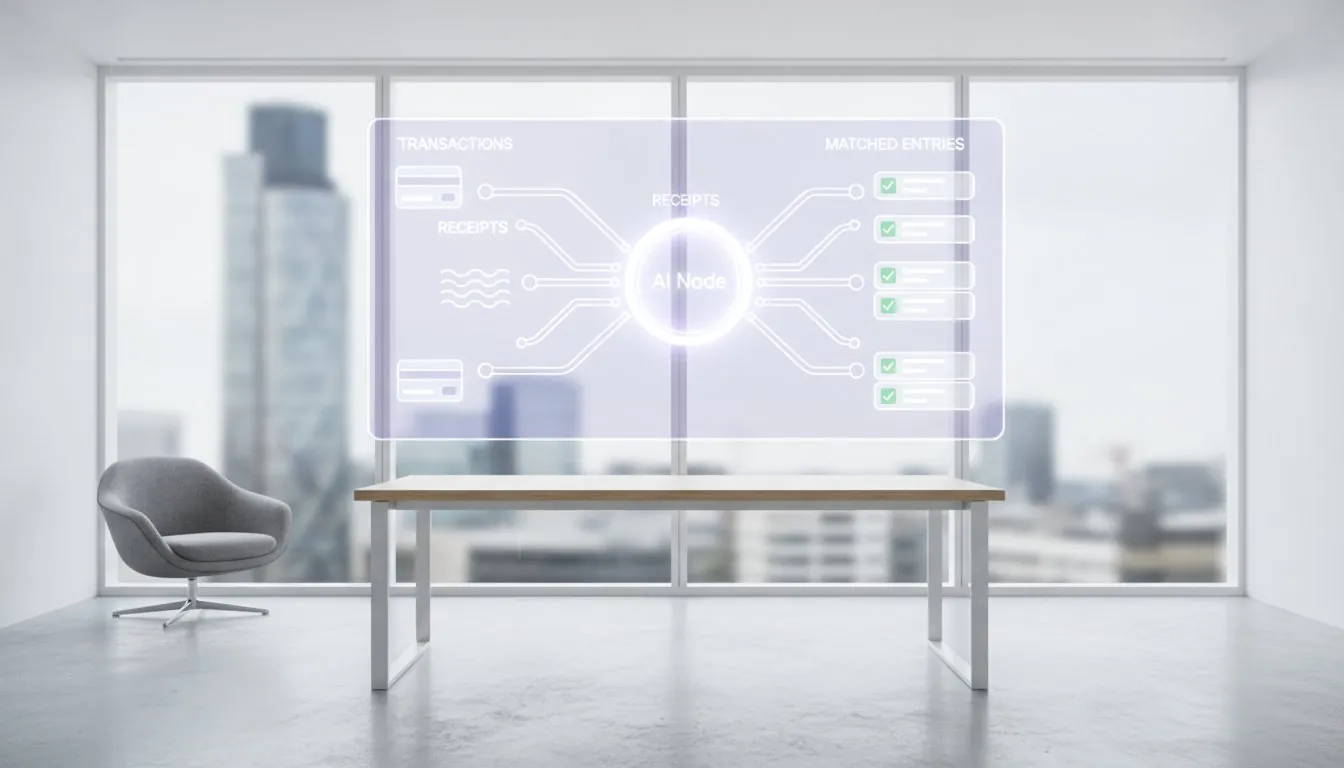

The transition from manual matching to AI-driven workflows represents a fundamental shift in how finance teams operate. Traditional software relies on rigid rules that often break when a vendor changes their billing format or a transaction amount fluctuates slightly. Modern automated credit card reconciliation software moves beyond these “if-this-then-that” constraints by employing intelligent pattern recognition. This technology doesn’t just look for matching numbers; it understands the underlying behaviour of your corporate spend, identifying relationships between entities that traditional tools would overlook.

Central to this advancement is the role of Natural Language Processing (NLP). This allows finance leaders to “train” their AI accountant using standard conversational English rather than complex code. If a specific vendor frequently bundles service fees with product costs, you can simply instruct the system to recognise this behaviour. This level of customisation ensures the software adapts to your specific business logic, rather than forcing your team to adapt to the software’s limitations.

From Rule-Based Matching to Intelligent Learning

The primary advantage of machine learning in this context is its ability to handle nuance. Whilst older systems might flag every minor discrepancy as an error, AI assigns “confidence scores” to matches based on historical data and vendor profiles. Research into the costs associated with credit card payments highlights that the administrative burden of processing these transactions often exceeds the transaction fees themselves. By automating the identification of anomalies, you can drastically reduce this overhead. For a deeper look at these shifts, see our AI Accounting in 2026: The Strategic Guide for UK Finance Leaders.

Open Banking: The Secure Foundation of Modern Finance

The fluidity of this process relies on the real-time data provided by Open Banking feeds. Unlike the clunky CSV imports of the past, API-based connections create a secure, direct bridge between your corporate card provider and your ERP system. This ensures data integrity is maintained at every step, removing the risk of duplicate entries or missed transactions. By acting as a Productivity Partner, the AI handles 95% of routine matches, leaving only the complex exceptions for human oversight.

This shift enables the “continuous close” model. Rather than a week-long scramble at the end of the month, automated credit card reconciliation software matches transactions daily. This provides the CFO with a real-time view of cash flow, allowing for agile decision-making based on yesterday’s spend, not last month’s. Exploring how AI reconciliations can integrate with your current workflow is the key to unlocking this level of operational clarity.

Essential Features for Choosing the Right Reconciliation Platform

Selecting the right automated credit card reconciliation software requires a shift in perspective. It’s not just about finding a tool that matches rows; it’s about finding a platform that integrates seamlessly with your existing financial architecture. If your software doesn’t “speak the same language” as your general ledger, you’ll simply replace one manual bottleneck with another. High-growth UK businesses need a solution that offers more than surface-level connectivity, ensuring that data flows without friction between corporate cards and the heart of the finance function.

Accuracy in receipt capture is the first line of defence against data fragmentation. Modern OCR (Optical Character Recognition) technology has advanced significantly by 2026, moving beyond simple text reading to contextual understanding. This means the software can distinguish between a VAT amount and a total balance even on faded thermal receipts. Furthermore, for organisations operating across borders, multi-currency support is vital. Your platform should handle automated FX variance calculations, ensuring that international spend doesn’t result in a week of manual adjustments during the month-end close. Customisable approval workflows then ensure that whilst the heavy lifting is automated, human oversight remains firmly at the centre of the process.

Integration and Ecosystem Compatibility

When evaluating potential platforms, you must distinguish between native “sync” and basic “import” capabilities. A native sync ensures that your automated credit card reconciliation software and your accounting system are always in lockstep, preventing the “data lag” that plagues older systems. For those using Sage, it’s essential to choose a partner that understands the specific nuances of that ecosystem. You can explore how this works in our guide to Sage Accounting Automation: The 2026 Strategic Guide for UK Finance Teams. A unified dashboard that aggregates data from Amex, Revolut, and high-street banks into a single view is the ultimate goal for real-time spend oversight.

Security, Governance, and Audit Trails

In the current regulatory climate, security isn’t a “nice-to-have” feature. Your chosen platform must be GDPR compliant and utilise enterprise-grade encryption to protect sensitive corporate data. Beyond encryption, look for an immutable audit trail. Every reconciled transaction should have a permanent, unchangeable record of its journey from swipe to ledger. This level of transparency is what makes a business audit-ready at a moment’s notice. Finally, evaluate the “human-in-the-loop” features. These safeguards allow your team to verify high-risk transactions, preventing AI hallucinations and ensuring that the final accounts are as reliable as they are fast.

How to Automate Xero Bank Reconciliation: A Step-by-Step Implementation

For UK finance teams, Xero is often the heart of the ledger, but its standard bank rules can struggle with the complexity of corporate card spend. Implementing automated credit card reconciliation software as an intelligent layer on top of Xero allows you to move from manual matching to strategic oversight. This isn’t a complex IT project; it’s a logical progression that begins with secure data flows and ends with a “soft-close” that takes minutes rather than days. By following a structured implementation, you can ensure your data remains audit-ready whilst your team focuses on high-value forecasting.

- Step 1: Connect via Open Banking. Establish a direct, API-based connection between your corporate card provider and your AI platform. This ensures every transaction is captured in real-time without the risk of duplicate entries or data gaps.

- Step 2: Map your Chart of Accounts. Sync your Xero nominal codes and tracking categories. This ensures that when the AI identifies a transaction, it knows exactly where it belongs in your specific ledger structure.

- Step 3: Instruct your AI Accountant. Use natural language commands to set your initial logic. You might tell the system: “Always categorise Adobe transactions as Software Subscriptions and apply 20% VAT.”

- Step 4: Centralise Receipt Capture. Encourage your team to upload receipts via mobile app or forward them via email. The AI will use OCR to match these documents to the bank transactions automatically.

- Step 5: Perform the Daily Review. Instead of waiting for month-end, review exceptions daily. This “soft-close” ensures your data is always current and takes under five minutes to complete.

Mapping and Logic Configuration

Success with Xero automation depends on how well you organise your tracking categories. By aligning these categories with your AI automation rules, you ensure that spend is not only categorised by nominal code but also attributed to the correct department or project. The software handles the granular details of VAT application based on vendor type and transaction value, significantly reducing the risk of HMRC audit red flags. If you’re ready to streamline this process, you can automate your Xero reconciliations today to achieve total visibility over corporate spend.

Optimising the Feedback Loop

The true power of automated credit card reconciliation software lies in its ability to learn. When you correct an occasional outlier, the system remembers that adjustment for future transactions. This creates a feedback loop that constantly improves accuracy without requiring you to write complex new rules. Your team’s role shifts from “doing” the reconciliation to “reviewing” the output, allowing them to focus on the business’s financial health. For a comprehensive look at this transition, read our guide on How to Replace Manual Reconciliation with AI: A 2026 Guide for UK Finance Teams. This shift in behaviour is what enables a finance function to scale without increasing headcount.

Beyond Matching: Scaling Your Finance Team with autoMEE

Scaling a finance department in 2026 requires more than just hiring more hands; it requires a fundamental rethink of how data moves through your organisation. Most high-growth UK businesses reach a plateau where manual processes can no longer keep pace with transaction volumes. This is where automated credit card reconciliation software evolves from a simple tool into a strategic force multiplier. By deploying autoMEE, you aren’t just matching receipts; you’re building a scalable architecture that allows your finance function to grow in capability without a corresponding increase in headcount.

The strategic advantage of this shift becomes most apparent during high-stakes board meetings. Instead of presenting data that is already three weeks old, you have real-time spend analytics at your fingertips. You can answer questions about departmental budgets or project-specific costs with absolute confidence, backed by data that is reconciled daily. This level of visibility transforms the finance team from a reactive back-office function into a proactive business partner. Staff are liberated from the drudgery of data entry, allowing them to focus on higher-value tasks like forecasting, variance analysis, and cost optimisation.

The autoMEE Advantage: Natural Language and Deep Integration

The primary differentiator of the flowMEE platform is its accessibility. You don’t need to be a developer to “talk” to your accounting software. By using natural language, you can train the AI to understand the unique nuances of your business logic, ensuring that automation feels like a custom-built solution rather than a rigid “black box.” This approach ensures that your processes remain secure and compliant whilst significantly reducing the time spent on manual oversight. For a deeper exploration of these strategies, read our guide on Accounting Automation for CFOs: The 2026 Strategy for High-Growth Finance Teams.

Your Journey to a Frictionless Finance Function

Transitioning to an “automated by default” model doesn’t require a disruptive overhaul of your current operations. autoMEE is designed to sit as an intelligent layer over your existing Xero or Sage setup, meaning implementation is swift and non-invasive. The long-term ROI is clear: as your transaction volume grows, the cost per reconciliation drops, allowing your team to maintain a “continuous close” without added stress. The future of finance is human-governed but technologically driven, ensuring your experts remain in control of the strategy whilst the AI handles the routine. We invite you to book a personalised demo to see how your own data flows through the platform and discover the true potential of automated credit card reconciliation software.

Mastering the Future of Financial Control

The landscape of UK finance is shifting toward a model where speed and transparency are non-negotiable. By moving away from the fragile “spreadsheet trap” and embracing automated credit card reconciliation software, you position your team as a strategic partner rather than a back-office function. You’ve seen how AI-driven workflows and real-time Open Banking feeds can transform the month-end close from a frantic scramble into a streamlined, five-minute review. This isn’t just about saving time; it’s about reclaiming the mental space to lead your organisation forward.

autoMEE provides the security and precision required for this transition. Our platform is fully GDPR and MTD compliant, ensuring your data remains governed whilst integrating seamlessly with Xero, Sage, and QuickBooks. Supported by our UK-based expert team, you can scale your operations with total confidence. It’s time to replace friction with fluidity and focus on the insights that drive growth. Book a personalised demo of the autoMEE AI accountant today to see how we can accelerate your close. Your journey to a frictionless finance function is just one click away.

Frequently Asked Questions

Is automated credit card reconciliation software secure enough for sensitive financial data?

Yes, automated credit card reconciliation software is built with security as a primary objective, utilising enterprise-grade encryption and secure Open Banking APIs. Unlike manual spreadsheet methods, which are prone to data leaks and unauthorised access, these platforms provide a controlled environment for your sensitive financial data. All connections are read-only, ensuring that your actual funds remain untouched whilst the data flows securely into your ledger.

How long does it typically take to implement automated Xero bank reconciliation?

Implementation for Xero bank reconciliation typically takes a few hours rather than weeks. Because modern platforms use API-based Open Banking connections, the initial link to your corporate card provider is nearly instantaneous. The majority of the setup time is spent mapping your Chart of Accounts and establishing your initial logic, allowing you to begin processing transactions almost immediately without disrupting your current workflow.

Can the AI handle complex transactions like split VAT or multi-currency charges?

Yes, the AI is specifically designed to manage complex scenarios like split VAT and multi-currency charges that often baffle traditional rule-based systems. By training the AI on your specific vendor behaviours, it can automatically recognise when a transaction needs to be divided across different nominal codes. It also handles FX variance calculations, ensuring that international spend is reconciled accurately against your base currency.

Will I still need to manually check the reconciliation results every month?

You will no longer need to perform a line-by-line manual check; instead, your team moves to a “review by exception” model. The automated credit card reconciliation software handles the 95% of routine matches with high confidence. Your role shifts to overseeing the final output and addressing the few complex anomalies that the AI flags for human judgment, which significantly accelerates the month-end close.

What happens if the software identifies a transaction that doesn’t have a matching receipt?

When a transaction lacks a matching receipt, the software automatically flags it as an exception and can trigger automated reminders to the relevant cardholder. This removes the need for finance teams to manually chase staff across the business. The transaction remains in a “pending” state until the documentation is uploaded, ensuring your audit trail remains complete and compliant with HMRC requirements.

Does automated reconciliation software work with all UK business credit cards?

Most modern reconciliation platforms work with all major UK business credit cards, including high-street banks and neobanks like Revolut and Tide. This coverage is facilitated by Open Banking standards, which have become the universal bridge for financial data in the UK. This ensures you have a unified dashboard for all corporate spend, regardless of how many different card providers your business utilises.

Can I use natural language to change the matching rules as my business evolves?

Yes, the ability to use natural language to update matching rules is a key feature of the autoMEE platform. You don’t need to be a technical expert to evolve your automation logic; you can simply instruct the AI in plain English. As your business grows or your vendor list changes, you can adjust your categorisation rules on the fly to maintain high accuracy levels.

Is this software compliant with UK GDPR and HMRC Making Tax Digital (MTD) standards?

Absolutely, the software is fully compliant with UK GDPR and HMRC Making Tax Digital (MTD) standards. As a UK-based technology provider, autoMEE ensures that all data processing meets the rigorous requirements of the Financial Services & Markets Bill 2026. This gives finance leaders peace of mind that their move toward automation is grounded in the highest levels of regulatory governance.